In February 2023, the European Union (EU) agreed to set a price cap on Russian refined oil products at $100 per barrel. The EU also set the price cap on Russian crude oil at $45 after setting it at $60 per barrel in cooperation with the Group of Seven (G7) countries in early December 2022, according to a periodic review every two months.

The European decision aims to control energy prices generally and stop price fluctuations that have affected global markets since the Covid-19 pandemic and the following events, particularly the commodity supercycle and the Russian-Ukrainian war. Furthermore, the Europeans aim to cut off the funding sources from the Russian federal budget that funds the military operation in Ukraine. In 2021, Russia exported oil worth around $212.4 billion of its $492.3 billion total exports to the rest of the world.

In response, the Russian government issued a decree on December 28, 2022, prohibiting the export of crude oil and petroleum products to countries with imposed price caps. Europe is the third-largest oil importer in the world after China and the United States. Conversely, Russia ranks first on the list of suppliers to the European continent while ranking second worldwide regarding oil exports. Therefore, we track in this article how the price cap decision may alter the global energy transmission paths.

Energy Paths Between Russia and Europe

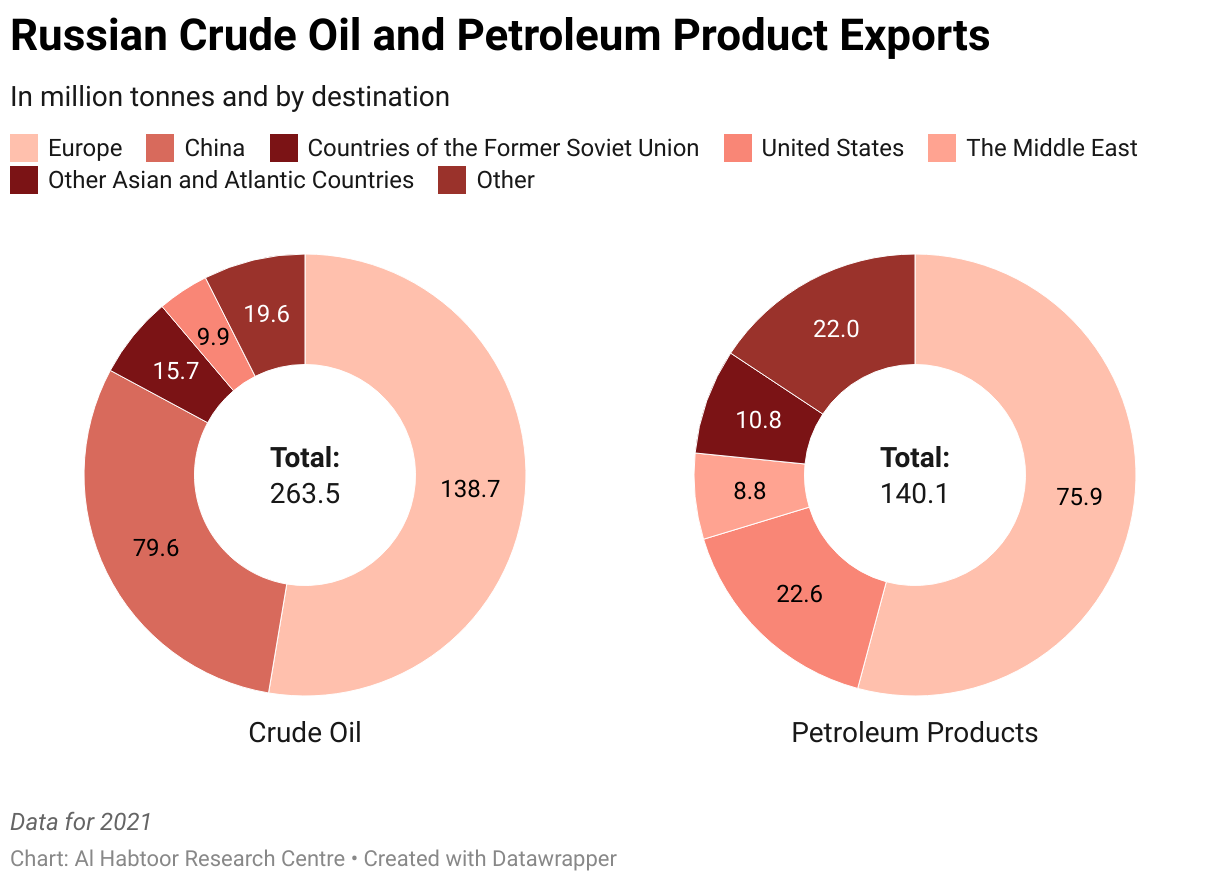

Before the military operations on Ukrainian territories, Russia’s oil exports were primarily sent to Europe as crude oil and petroleum products. In 2021, Russia exported 263.5 million tonnes of crude oil. Europe acquired most of it with about 138.7 million, 52% of the total Russian oil, followed by China with about 79.6 million tonnes, 30% of the total oil exports.

The same remains true for petroleum products, by-products of the processing and refining of crude oil, most notably gasoline, diesel fuel, and naphtha. Of the 140 million tonnes of Russian exports, Europe acquired 75.9 million tonnes, roughly 54% of the total, followed by the United States, with about 22.6 million tonnes, approximately 16% of the total Russian exports.

The following figure shows the distribution of Russian oil and petroleum products exports according to their destinations in 2021, i.e. before the Russian-Ukrainian war:

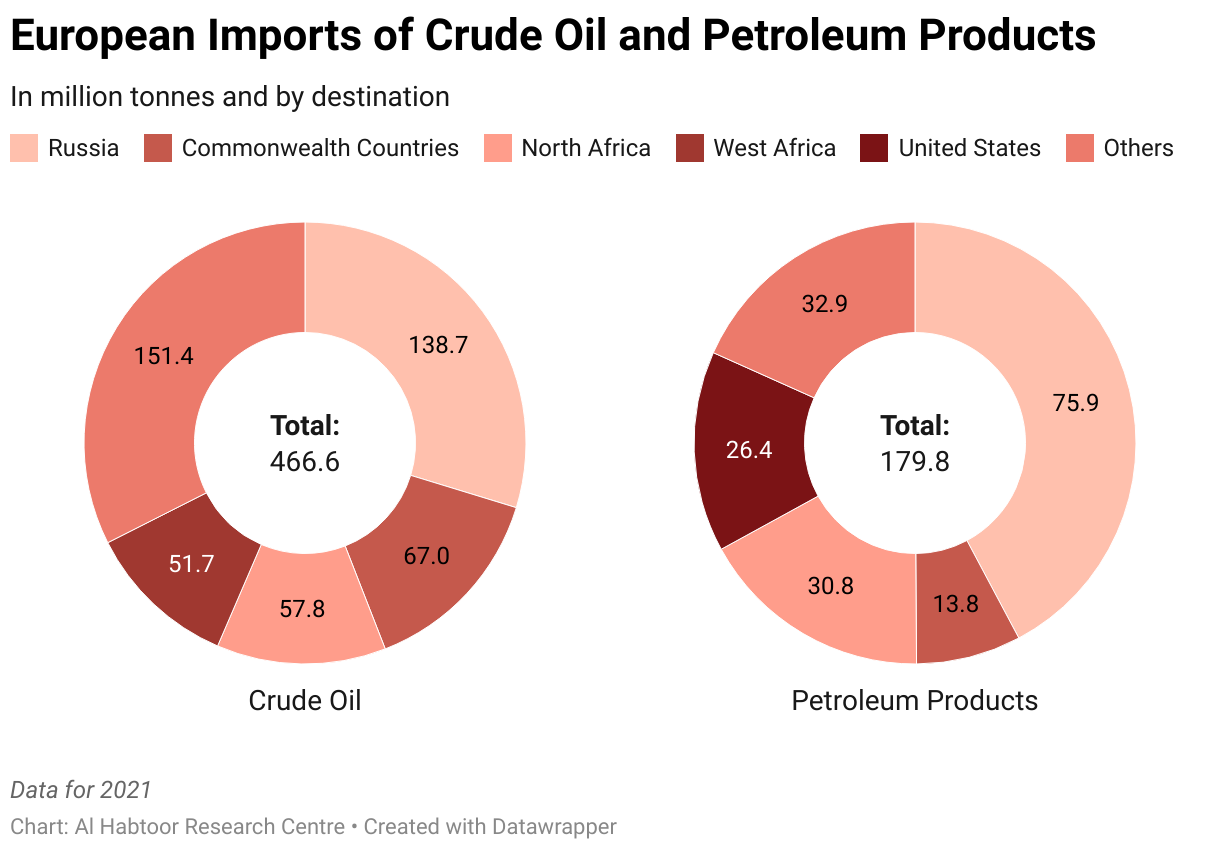

The same applies to the European continent, which relies on Russia as the primary supplier of oil and petroleum products. In 2021, Europe purchased 467.7 million tonnes of crude oil, of which 138.7 million tonnes came from Russia, making up about 27% of all imports. The United States came in second place with around 51.4 million tonnes, as shown below.

The same situation holds true for petroleum products’ imports. Russia tops the list of suppliers with about 75.9 million tonnes out of the total 197.5 million tonnes imported by Europe, accounting for 38% of the total imports, followed by the United States of America with about 26.4 million tonnes.

The European-Russian mutual dependence regarding trade in crude oil and petroleum products in light of the embargo imposed by Russia will push the two sides to find an alternative partner who is able to absorb the enormous quantities offered by the Russian side. Also, Europe will look for a substitute supplier to provide the massive amounts it received from the Russian side.

The paths of nearly 138 million tonnes of crude oil, representing roughly 13% of the global oil flow and about 12% of all petroleum products sold globally, would shift in both directions. Consequently, producers’ supply chains will generally be disrupted, and there will be an unprecedented high demand for tankers.

Disruption of Global Energy Paths

A shift in the oil pathways is unavoidable due to the deteriorating political relations between Europe and Russia and their mutual reliance on the oil trade, which forces both of them to look for alternatives. As a result, more tankers will be used to transport products between the two sides.

Oil Paths Shift

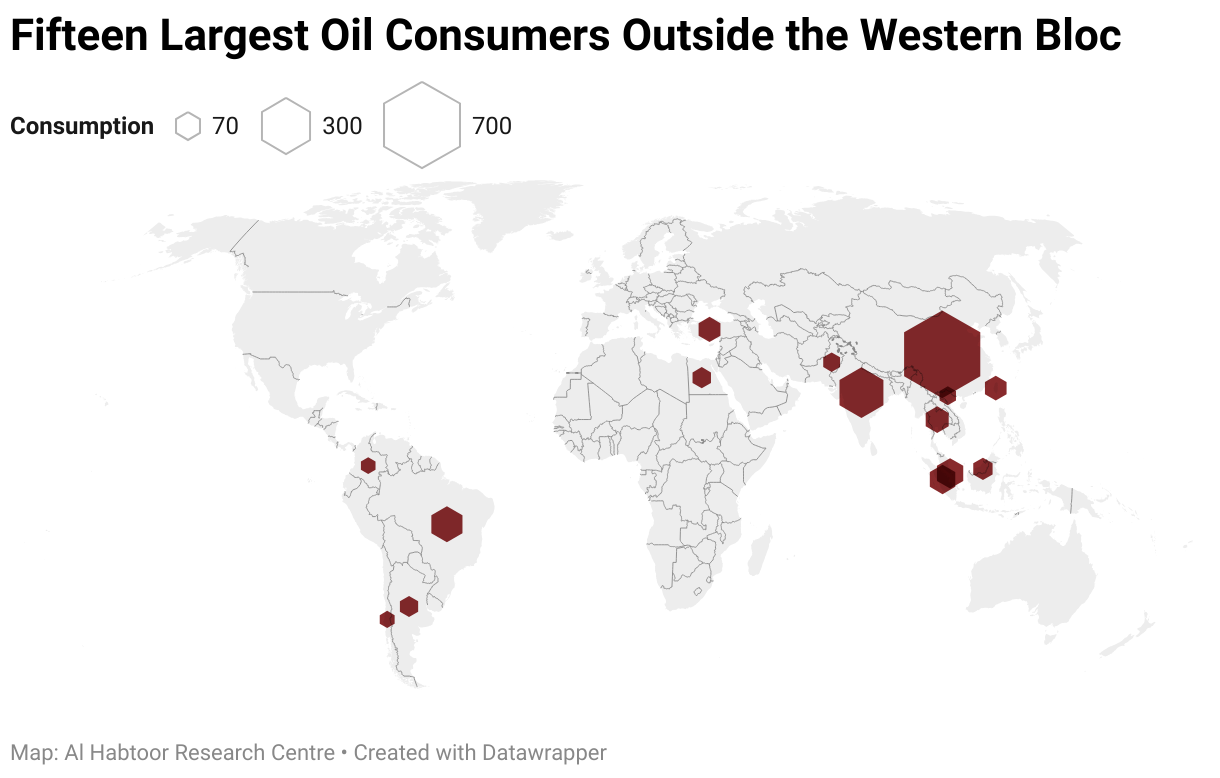

Russia’s quest for a substitute purchaser will inevitably lead to significant consumers beyond the Western bloc. This diminishes the available alternatives to few countries, namely India and China, as well as several other developing countries, including Egypt, Turkey, and Nigeria, all of which will welcome Russian crude and oil products. Russia now offers these products at huge discounts of up to 20% off the market price. The following figure shows the fifteen largest purchasers in the world, excluding the Western bloc and the most prominent exporters:

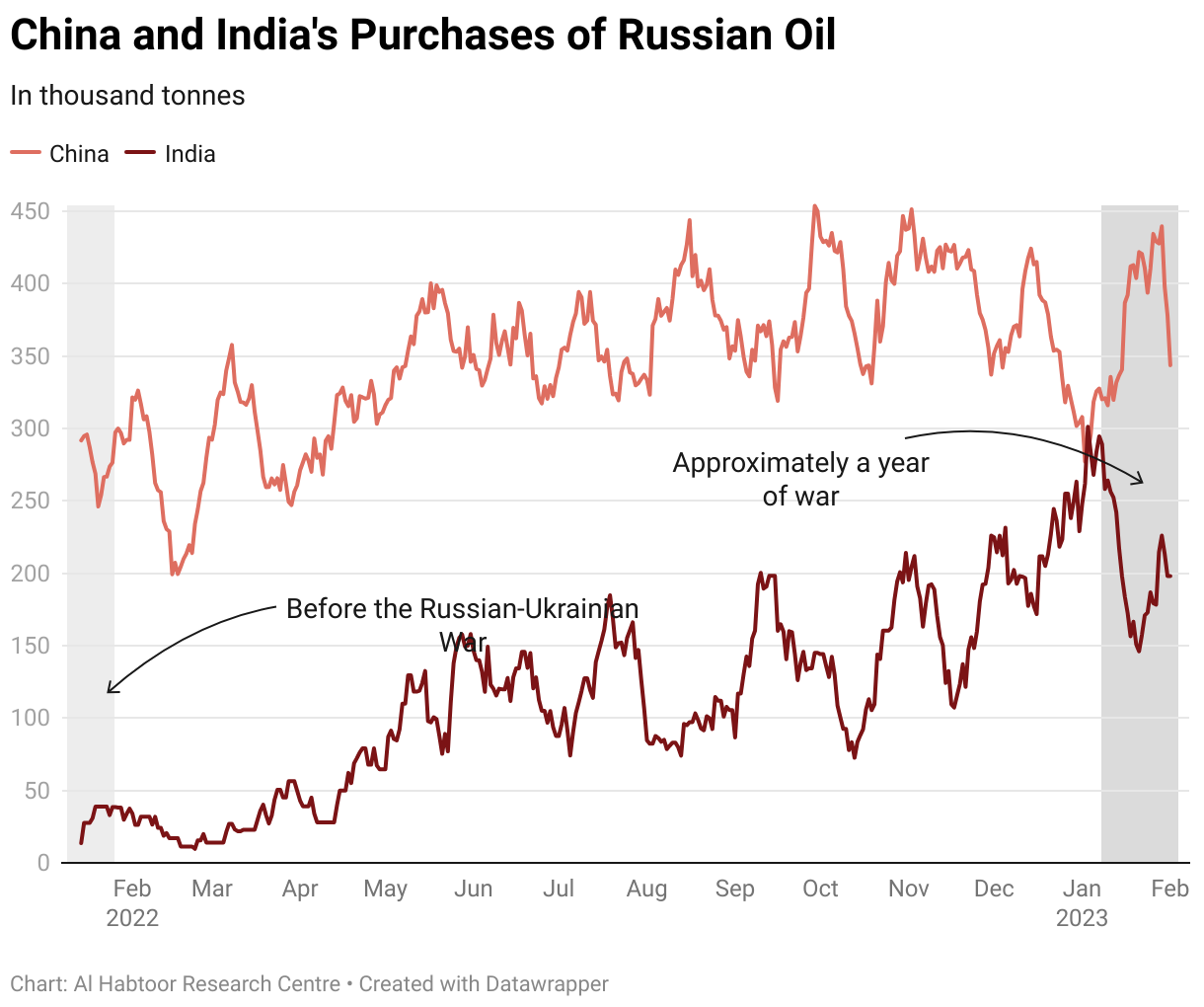

According to the figure above, all significant importers do not share geographic borders with Russia, except for Turkey and China, who are long term importers of Russian crude oil. This means the transmission lines between Russia, China, and Turkey are busy with exports. Therefore, Russia will have to use oil tankers to transport its products to one of these consumers, which is already happening. As a result, Currently, Chinese purchases of Russian crude oil and petroleum products increased from 291.7 thousand tonnes on January 14, 2022, to 343.7 thousand tonnes on February 1, 2023. Likewise, Indian purchases rose to 198,000 from 14,000 tonnes on January 14, 2022. The following figure shows the evolution of Chinese and Indian Russian crude oil and petroleum products purchases.

The figure reveals that between the beginning and conclusion of the period, Chinese purchases climbed by about 52 thousand tonnes, a rise of 18%, while Indian purchases increased by nearly 184 thousand tonnes. These amounts will be or have already been transported across the seas using oil tankers.

The scenario is the same in Europe, where efforts will be made to make up for the quantities lost from Russia, particularly in light of the embargo that Moscow would impose. This position makes more sense since the only oil producers that can supply the enormous European demand are confined to the countries of the Middle East, especially the Kingdom of Saudi Arabia and the United Arab Emirates, or the countries of North America, especially the United States of America. Accordingly, European quantities will arrive via tankers from the Middle East or North America.

Unprepared Fleet

Oil tankers are the only available method for transporting these enormous amounts of crude oil and petroleum products between the new parties. However, the industry was not ready for this new situation for two main reasons:

First: The general trend to abandon oil in favour of natural gas in the long term is the demand for the construction of Oil Tankers to LNG Carriers, which are only appropriate to fulfil the roles of the other.

Second: The logistics crisis that struck the world during the first three quarters of 2022 due to China’s closure of ports owing to precautionary measures against the new coronavirus pandemic caused hundreds of tankers to halt in front of the Chinese ports, raising the overall cost of shipping.

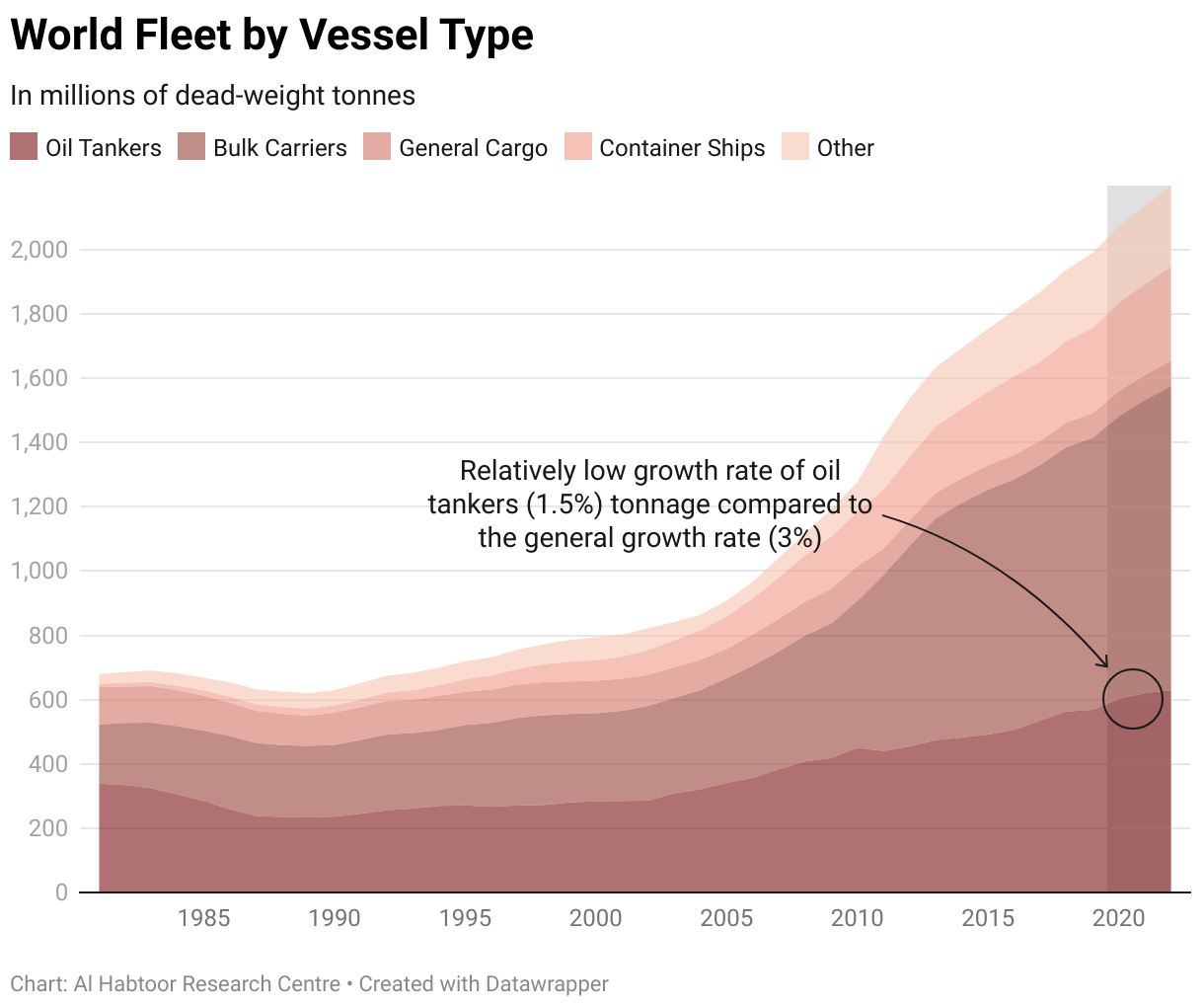

In terms of the overall state of the oil tanker industry, the new quantities put pressure on the industry. The total amount that the world’s fleet of oil tankers can transport is 629 million tonnes. On the other hand, the redistributed amounts total 426 thousand tonnes per day, an average of around 155.4 million tonnes in both directions annually, or 24% of the total tonnage available, as the following figure shows:

Losses for All

The previous turmoil will pressure the maritime transport industry, particularly oil transport. The most direct impact of these pressures is the high cost per tonne of oil delivered from Russia to Europe, whether over less expensive landlines and in less time or on-board oil tankers for short distances. As a result, oil would be carried long distances from the Middle East to Europe, often via the Suez Canal or across the Atlantic from the United States. The impact on India and China will be the same because they will receive Russian oil via the Canal route, or at the very least via the North Corridor route through the Arctic, with the minor exception that Russia will need to offer discounts to the two countries in order to persuade them to switch from their current suppliers.

Generally, the high price of oil is mirrored in the price of commodities. This is because energy, especially oil, is the primary driver of economic activity. As a result, European products will be less competitive on global markets than their American equivalents, made using inexpensive domestic oil, or Chinese products, produced using Russian oil at a discount of around 20%. However, the Russian side incurred huge losses because it routinely guaranteed the sale of its products to neighbouring European countries without discounts and at a low cost of transportation compared to the price it would bear in the future.

This affects the global economy due to the general increase in energy material costs driven by the massive demand for them in Europe. Furthermore, there would be an overall rise in price levels, which would raise the inflation rate and pressure the world economy, especially the developing countries that suffer from the compound effects of rising commodity prices globally and high-interest rates, which worsen hunger, poverty, and unemployment worldwide

References

EU agrees on price caps on Russian refined oil products | Reuters [Internet]. [cited 2023 Feb 7]. Available from: https://www.reuters.com/business/energy/eu-agrees-price-caps-russian-oil-products-2023-02-03/

Statistical Review of World Energy | Energy economics | Home [Internet]. [cited 2023 Feb 7]. Available from: https://www.bp.com/en/global/corporate/energy-economics/statistical-review-of-world-energy.html

Putin bans Russian oil exports to countries that implement price cap | Reuters [Internet]. [cited 2023 Feb 7]. Available from: https://www.reuters.com/business/energy/putin-bans-russian-oil-exports-countries-that-imposed-price-cap-decree-2022-12-27/

Russia Fossil Tracker – Payments to Russia for fossil fuels since 24 February 2022 [Internet]. [cited 2023 Feb 9]. Available from: https://www.russiafossiltracker.com/

Beyond 20/20 WDS – Table view – Merchant fleet by flag of registration and by type of ship, annual [Internet]. [cited 2023 Feb 9]. Available from: https://unctadstat.unctad.org/wds/TableViewer/tableView.aspx?ReportId=93

Related Articles

Larijani’s Visit: Building Alliances or Rescuing Allies?

Middle East in Energy Transition: From Stopgap to Global Architect

What If: The Middle East Burns Next?

AI’s Crossroads: Decoding the Middle East’s AI Transformation

What If: As-Suwayda Sought Independence?

Pulse: Nuclear Risk in the Middle East

From Isolationism to Intervention: Trump’s MENA U-Turn

Iran’s Enriched Uranium: Potential Flashpoint for Renewed Conflict

What If: Iran Attacked the Dimona Reactor?

What If: The India-Pakistan Ceasefire Collapses?

Is the Russia-Ukraine War Nearing Its End?

Making Sense of Trump’s Foreign Policy

The Core Issue: Ammunition Manufacturing and its Effects on the Russia-Ukraine War

Are the Paris Olympics Too Political?

Has Moscow’s Control Over Europe Become Uncontrollable?

Macron’s War Rhetoric and his Desperate Quest for Prestige

Turkey: Reaping the Rewards of a Turbulent Black Sea

BRICS’ Future Currency and the Global Financial System

New Gulf: Russo-Ukrainian War and Emergence of North Africa’s Energy Sector

Comments